Shares delicately poised

Published 17 August 2010 in the ASX Newsletter by Dale Gillham

The market could be starting a 30-year bull run - but more falls are likely in the short term. Too many investors focus on daily market movements and react to market noise instead of real market movements. But it has been shown repeatedly that traders make more money with less effort by concentrating on the bigger picture. The important question is not why the market has moved up or down today, but where is it likely to be heading over the medium term?

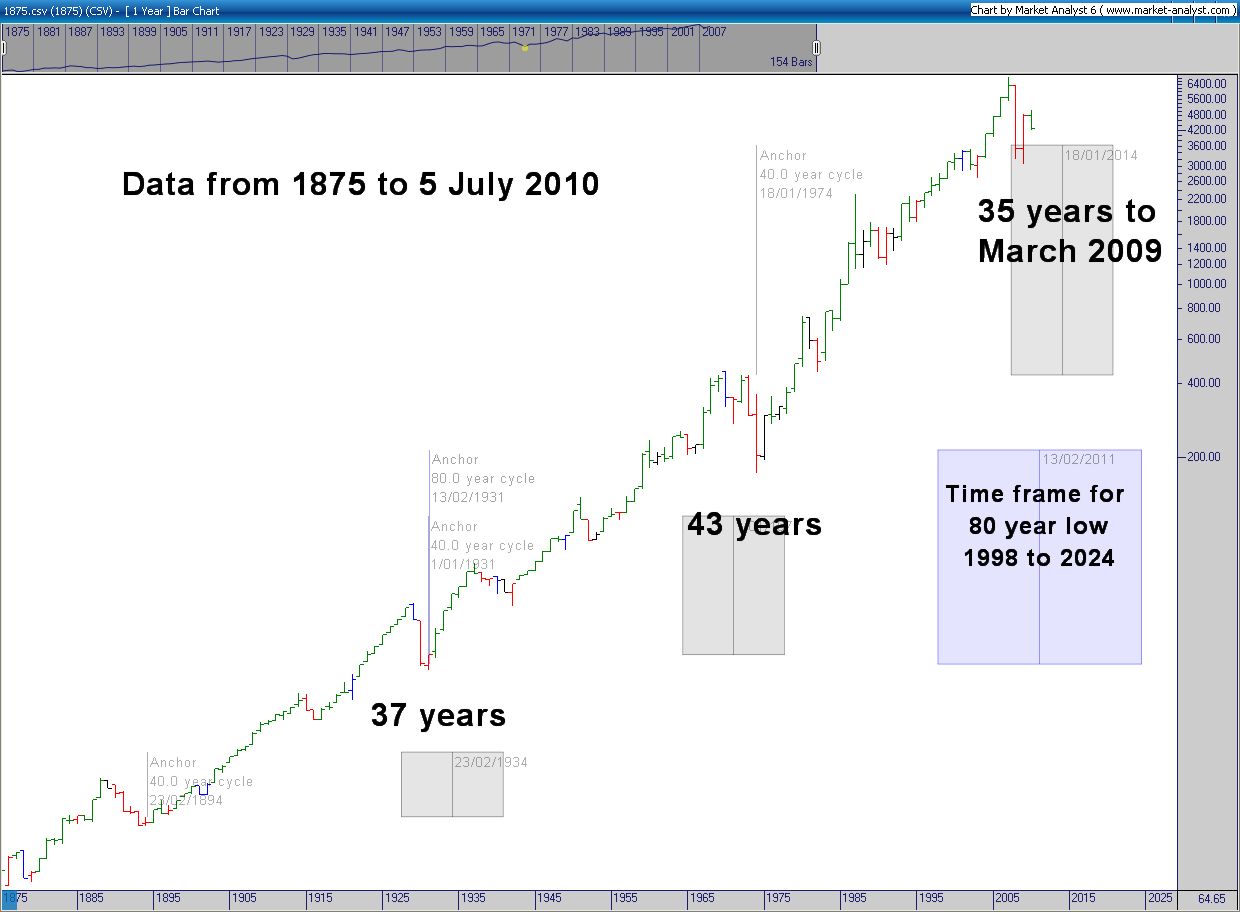

Figure 1, below, is the yearly bar chart of the All Ordinaries index dating back to 1875, on which I have placed some long-term time cycles. Notice the market fell into a long-term low in 1894 to end a five-year bear market, with the decline around 40 per cent. Thirty-seven years later (into 1931) the All Ordinaries Index experienced a two-year bear market and a fall of slightly over 50 per cent between 1894 and 1921. Moving forward 43 years, we see a four-year bear market decline into 1974 of greater than 61.8 per cent. Lastly, 35 years on, the market pulled back into March 2009 for 18 months and just over 50 per cent.

Given these statistics, can we make a case to suggest the bear market has finished? Historical data supports this view, but it can also be argued that the bear market may still be unfolding.

Figure 1: All Ordinaries yearly bar chart dating back to 1875 Click to enlarge

Time is on market's side

The Australian share market is in the time-probability box for the low, but March 2009 is only 35 years from 1974, so we need to consider that the market could fall further into a low between 2011 and 2017 and still be consistent with the time frames of the last two long-term lows. Although the fall into March 2009 is consistent with previous falls, it could continue to 61.8 per cent (2724 points) and still fit past cycles. Given this, I suggest our market may fall further in both time and price, and therefore it is wise to consider this in your investment decisions.

That said, we could also be at the start of the next 30-year-plus bull market. I cannot confirm this until the 2007 high has been broken, so I am erring on the bearish side. But as I always say plan for the worst and hope for the best.

S&P 500 has relatively short history

Let us look at the US market indices, the Dow Jones Industrial and the S&P 500. The Dow comprises the top 30 US companies; the S&P includes the top 500. Therefore, the thought is the S&P is a better comparison for the All Ords than the Dow. However, the S&P did not begin until the 1950s and available data only goes back to the 1970s. This is not enough history from which to draw a reasonable conclusion. Although not shown, if you overlay a chart of the S&P and Dow you will notice they are very similar in form and that significant lows occur at the same time, therefore enabling comparisons between the Dow and the All Ords.

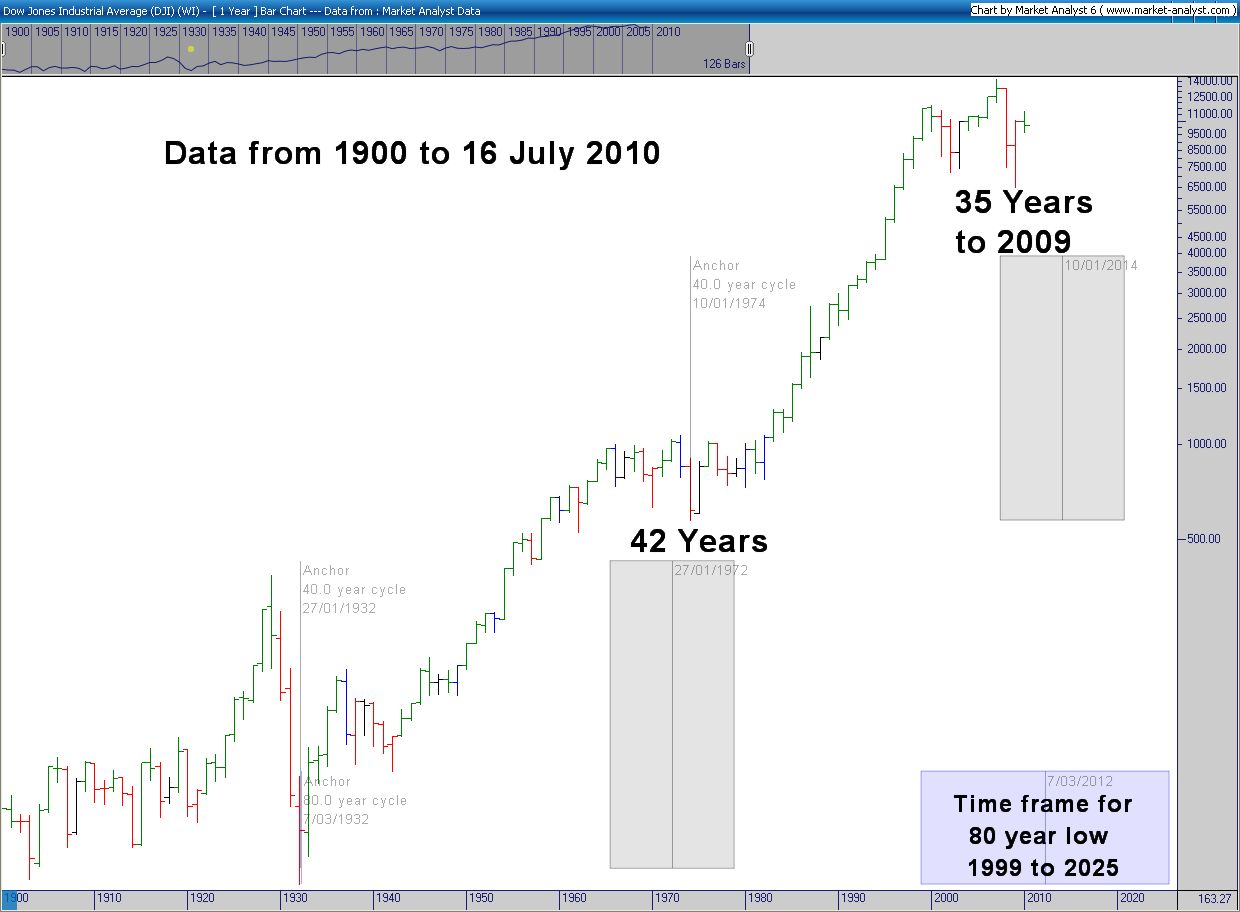

Figure 2, below, shows the Dow from 1900 to 2010. There are similar long-term movements as for the All Ordinaries Index in Figure 1, above. That said, often the time of the low and degree of each fall can be quite different. For example, the Dow fell approximately 90 per cent in price over three years into 1932, then 42 years later it fell over about 18 months and 50 per cent in value into 1974. Both downward moves were very different from what occurred on the All Ordinaries Index, in time and price. Thirty-five years later, we see a decline of 50 per cent and 61.8 per cent over 18 months into the March 2009 low.

Given the above figures, it is possible the Dow, like the All Ordinaries Index, has further to fall in both time and price. If so, one scenario is the Dow falls to around 5775 points or below over the next few years. The range in time for the low is between 2007 and 2021, with probability suggesting the low by 2016. This view fits with our view that the Australian market may fall over the next few years.

Figure 2: Dow index from 1900 to 2010 Click to enlarge

Supporting this view is the next chart of the S&P 500 index (Figure 3). While the Dow made a significantly higher top in 2007, the S&P formed what I consider to be a double top. Theory states that after such a pattern has formed, it is possible for the market to fall to between 150 and 250 per cent of the range from the high of March 2000 to the October 2002 low, projected downwards from the October 2007 high. Given this, we find a target of around 5000 points on the Dow, which is near the level mentioned above at 5775 points, and a target of about 400 points for the S&P 500.

Figure 3: S&P 500 index from 1977 to 2010 Click to enlarge

Short-term caution on the All Ordinaries

As mentioned, plan for the worst and hope for the best. Now we can look at how the market is likely to unfold if the March 2009 low is the longer-term low. History tells us that our market takes an average 41 months to return to the previous all-time high after a bear market. Therefore, the time target for the All Ordinaries Index to break the previous record of 6873 points is around September 2012, but it could occur earlier.

In the short term, I believe the All Ords still has the potential to pull back to between 3800 and 4000 points into September 2010, and if the bear market has concluded we could reasonably expect to see it rise to between 5500 and 6000 points over the coming year. I believe volatility will remain high for at least the next six months and therefore, no matter what your view of the market, it is critical to set stop-losses to protect capital.

Last fact checked 25 October 2018

Back to Articles