3 ASX IPO’s You Can Buy Cheaper Today: Huge Upside

By Fil Tortevski and Pedro Banales

While the world focuses on the mega IPO season unfolding in the US right now, including the upcoming SpaceX listing, we have dug through our own market to uncover three ASX stocks that recently IPOed and can now be bought far cheaper than their listing price. The technical setups are compelling, and these names have the potential to skyrocket from here, provided you know exactly what to look for before it happens.

In the latest episode of the Hot Stock Tips Show, Filip Tortevski and senior analyst Pedro Banales walk through three Australian listings that have followed the classic post-IPO drawdown pattern, where statistics show that six to twelve months after listing, you can often pick up quality businesses at materially better prices than the initial hype allowed.

Why Recently Listed ASX Stocks Often Trade Cheaper than at IPO

The pattern across IPOs is remarkably consistent. A new listing typically experiences an initial spike driven by hype, followed by a fade as reality sets in and the early speculative buying gets exhausted. This is why most professional traders ignore the first four to five weeks of any new listing, because that period is purely sentiment-driven rather than indicative of genuine value.

What matters is what happens next. When a stock has fallen well below its IPO price, consolidated, and started showing signs of accumulation through higher bases, weakening selling pressure, and rising volume on up moves, that is when the real opportunity emerges. All three of the stocks discussed in this episode currently sit in exactly that zone.

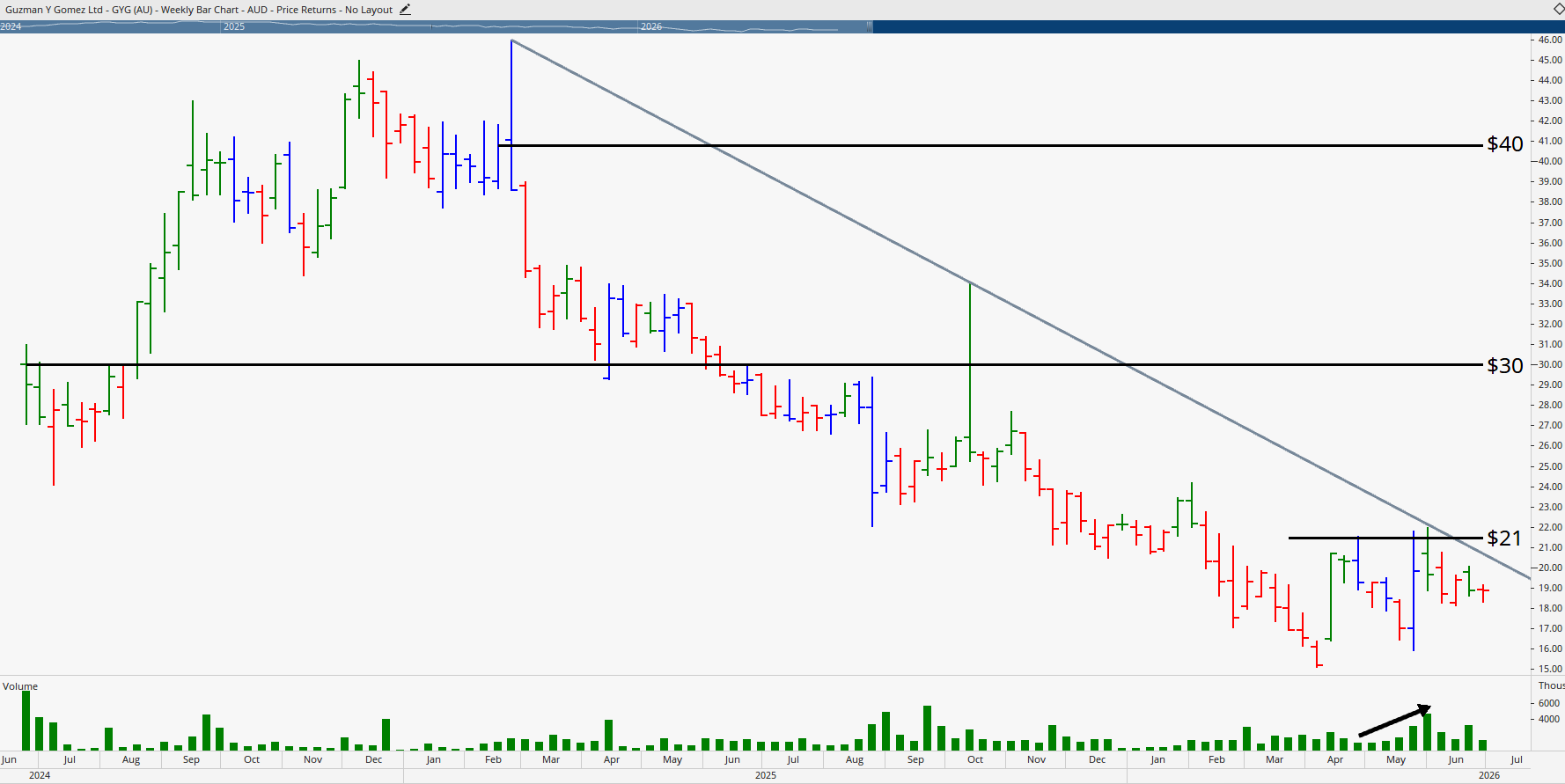

1. Guzman y Gomez (GYG)

Guzman y Gomez listed in June 2024 at around $30 with all the typical IPO euphoria. The initial spike failed, the stock began rolling over, and the signs were visible in the price action well before the major correction unfolded. Today, the share price tells a very different story, and the technical setup is genuinely interesting.

The bull case for GYG rests on several fundamental drivers. The company is rolling out approximately 30 new stores annually, same-store sales growth is supporting demand, and importantly, management has cut losses in the loss-making US business. This kind of decisive action, where a company quickly exits an underperforming market rather than burning capital trying to make it work, is exactly the kind of catalyst that can revalue a stock significantly.

The Technical Setup

The weekly chart shows the IPO price was around $30, followed by major selling that drove the price well below the listing level. In late October 2025, buyers attempted a recovery only to be sold off immediately, with the close near the week's lows. Fast-forward to today, and the picture has shifted. The runs down are getting smaller, the buying pressure into supports is getting stronger, and the 10 April close was particularly strong with sellers failing to push the price lower.

If the stock holds above the recent low from 22 May, that gives three confirmation signals working together. Higher prices, weakening sellers, and the kind of base-building pattern that often precedes a meaningful reversal. Volume supports the bull case, with up moves attracting stronger participation and pullbacks coming on lighter volume.

The key level to break is $21-$22, which marks the high from 29 May. A clean break above that opens the path back to the IPO price around $30, representing roughly 50% upside from current levels. Longer term, if the turnaround story plays out properly, the $40 region where the initial euphoria peaked becomes a realistic target, though investors should focus on the IPO level first as the more achievable risk-reward play.

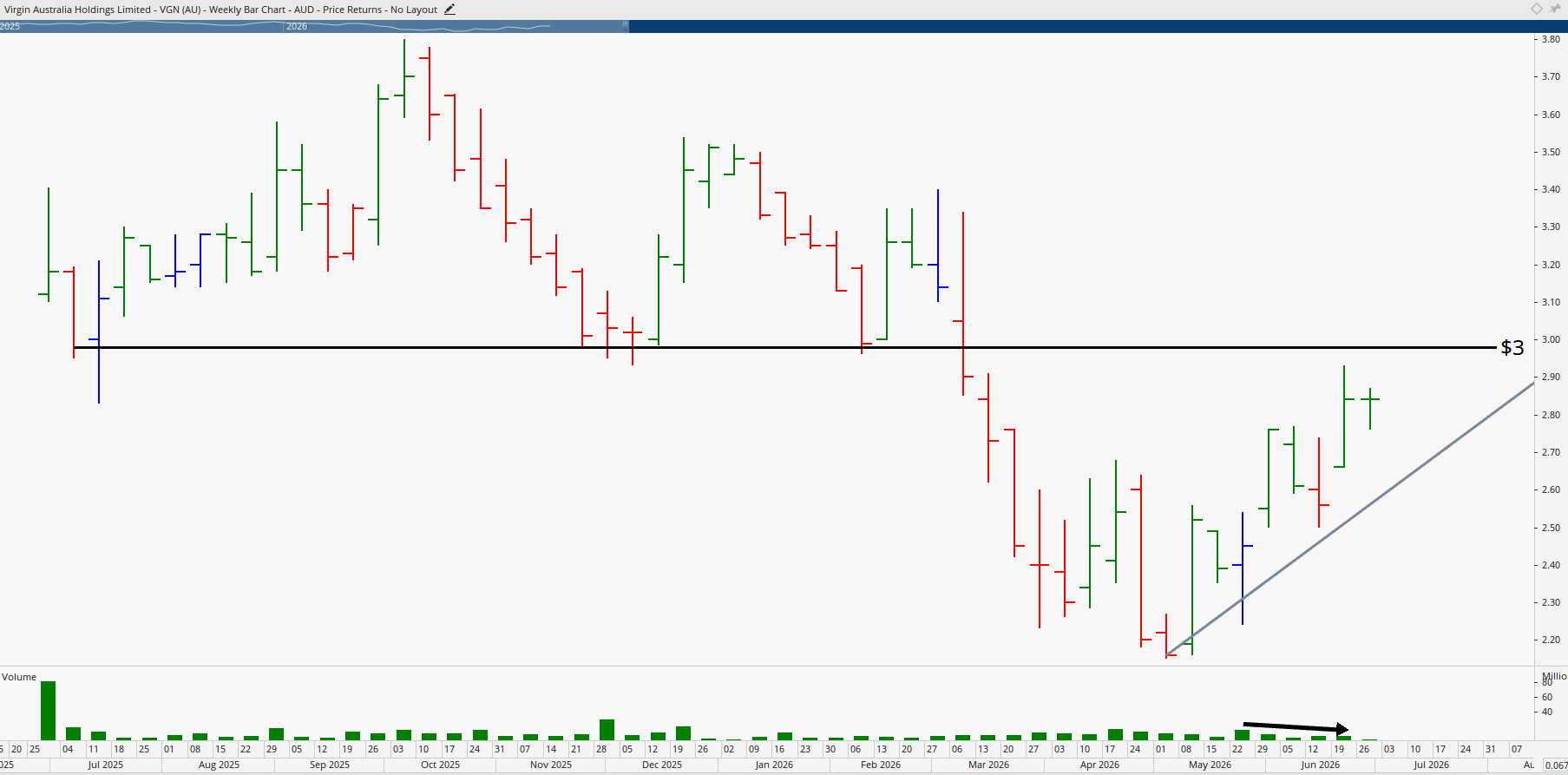

2. Virgin Australia (VGN)

Virgin Australia is Australia's second-largest airline and the owner of the Velocity frequent flyer business. What makes this listing particularly interesting is that the chart, despite Virgin having far less listed history, moves remarkably in sync with Qantas. If you have a positive view on the broader airline sector, Virgin offers an alternative angle with potentially more upside given how heavily it sold off post-listing.

The bull case rests on growth in the high-margin Velocity loyalty business operating separately from the airline, lower fuel prices boosting profitability, and the potential for the market to eventually value Velocity as a separate asset rather than lumping it in with the airline operation. With oil falling from highs near $110 to the $70s and supply-demand fundamentals remaining bearish, fuel costs could continue to ease, directly supporting airline margins.

The Technical Picture

The IPO price was $3.11. The market initially rose to around $3.20 to $3.30 before topping out near $3.40, suggesting that level represents the upper boundary of where the market is currently willing to pay. From today's price, that still offers around 22% upside to the previous high zone.

The longer-term setup shows the longest sustained run since listing, with higher bases printing on multiple occasions for the first time. The stock has broken above the $2.60 congestion zone, where buyers had previously failed multiple times, which is a constructive signal. However, the $3 level represents the next major resistance, and with volume falling as price rises, there is reason for caution. Qatar Airways holds a 25% stake, and disruptions in the Middle East, along with the company's debt position, add complications.

This one is more of a watch than an immediate buy. If $3 breaks cleanly, the path opens to $3.40 with around 13% upside in the medium term. If the stock fails at $3 and pulls back, the gap near $2.56 remains as a logical retest level. Either way, the technical structure has improved meaningfully from the post-IPO collapse.

3. Plenti Group (PLT)

Plenti is the pick of the bunch from a setup perspective. The company is a technology-driven private credit lender providing car loans, renewable energy financing including solar, and personal loans. With private credit growing 21% annually since 2015 and traditional banking starting to wane in this space, Plenti operates in one of the more attractive growth segments of the financial services sector.

The bull case here is essentially a pure interest rate cut play. Falling rates reduce funding costs, support demand, and improve margins on the existing loan book. With the RBA holding rates at its most recent decision and consensus pointing toward an easing cycle starting later in the year, Plenti is exceptionally well-positioned to benefit if the rate cut narrative plays out.

Why 66 Cents Is the Critical Level

The 66-cent level has been one of the most important technical zones for this stock since the IPO at around $1.40 back in September 2020. The strongest evidence of major buying came in November 2023, where price held without even pulling back to retest, which signals serious institutional interest rather than a flash-in-the-pan move. The stock has now spent over two years respecting this level on multiple tests, and the most recent test saw buyers step in immediately, with price already recovering to 78 cents.

Looking at the historical performance, when interest rates were moving in 2021, Plenti rallied. When rates moved again from 2023 to 2024, the stock rose 400%. The setup is repeating now, with rates poised to move in the opposite direction, creating a similar catalyst-driven opportunity.

How to Trade Plenti

This is best treated as a medium-term trading opportunity rather than a buy and hold. The first resistance sits at $1, which has previously acted as both support and resistance, representingaround 20% upside from current levels. The major ceiling sits at $1.60, where significant prior price action has clustered. A simple momentum line drawn across the recent peaks provides a logical breakout trigger for entries.

Volume is starting to pick up on up moves, with a notable spike on the recent rise and lighter volume on the pullbacks. The June low around 73 cents is the critical support level to watch. If that holds and the stock continues to print higher bases above the immediate momentum line, this could be on the verge of a meaningful move. The risk-to-reward equation needs to be assessed on an individual basis, but the combination of fundamental tailwinds and technical structure makes this the standout name among the three.

The Lesson: Patience Pays With IPOs

What links all three of these stocks is a simple principle. New listings rarely represent the best entry point. The hype-driven initial spike sets the high-water mark, and the months that follow often reveal far better prices for patient investors who understand price action and wait for confirmation.

The skill lies in identifying the moments when selling pressure weakens, buying steps consistently at key levels, and the price action shifts from distribution to accumulation. This is exactly what we focus on at Wealth Within. Our share trading education is built around teaching you how to identify these setups for yourself, so you are never reliant on someone else's view to make confident decisions.

For those starting out, the Short Course in Share Trading provides the foundational skills needed to read charts, manage risk, and trade with structure. If you are ready to commit to a comprehensive, government-accredited program, the Diploma of Share Trading and Investment teaches the full five-step approach for becoming consistently profitable. And for graduates wanting to refine their edge with techniques like time analysis and Elliott Wave, the Advanced stock trading course is the natural next step.

Final Thoughts

Three recently listed ASX stocks, three different sectors, and one common technical theme. Each has fallen well below its IPO price, each has spent meaningful time consolidating, and each is now showing the kind of structural improvement that often precedes a sustained recovery. Guzman y Gomez offers a turnaround story with around 50% upside to the IPO level. Virgin Australia provides exposure to falling oil prices and the Velocity loyalty business with around 22% upside to recent highs. Plenti stands out as the strongest pure rate cut play with 20% upside to first resistance and far more if the broader rate easing cycle materialises.

As always, the difference between catching these moves and watching them pass by comes down to skill, structure, and discipline. Identify the levels, wait for confirmation, and manage your risk. With the right education and approach, opportunities like these become far easier to act on, with the certainty needed to commit capital.

Disclaimer: This article is general in nature and does not constitute personal financial advice. Always conduct your own research or consult a licensed adviser before making investment decisions.