Big Dividends, Big Growth: This Doesn't Happen Often

By Dale Gillham, Janine Cox and Fil Tortevski

Huge dividends and massive growth at the same time. Can you really have both? Most of the time, the answer is no, but right now several carefully selected ASX stocks are offering exactly that combination. With long-term technical structures sitting at major support levels and yields well above the market average, this is the kind of setup income investors rarely encounter.

In the latest episode of the Australian Stock Market Show, Chief Analyst, Dale Gillham, and senior analysts Janine Cox and Filip Tortevski work through how to think about income portfolios properly, why chasing the highest yield is one of the most dangerous habits an investor can develop, and which ASX stocks are setting up for both reliable dividends and meaningful capital growth.

How to Pick the Right Stocks for an Income Portfolio

The biggest mistake most investors make with income portfolios is treating yield as the first criterion. Going for the highest dividend yield, particularly anything in the 10% plus range, is usually a sign of risk rather than opportunity. Stocks paying the highest yields tend to be the most fragile, and a high yield often reflects a falling share price more than a generous payout policy.

The smarter approach is to look for stocks paying around the market average, broadly between 4% and 7%, with a track record of paying consistently through both booms and crashes. These are the businesses that survive market cycles and continue rewarding shareholders regardless of conditions. With the cycle moving toward a point where yield will be increasingly valued, building a portfolio around reliable players rather than headline yields is the foundation of long-term income success.

The second principle is even more important. Direction matters more than yield. A stock paying 11% that is in free-fall will destroy more capital than the dividend will ever return, while a stock with a moderate yield and a clean uptrend can deliver both income and capital growth. Always check the price action first, and only then decide whether the yield is worth pursuing.

Where the Best Income Plays Are Setting Up

The Australian market is currently sitting at fair value on most metrics, including three-year and five-year price-to-earnings ratios. This is materially different from the US, where certain segments are stretched to extremes. That means the whole ASX is potentially fertile ground for income investors, but some sectors stand out more than others.

Healthcare and real estate, both traditionally defensive sectors, have already corrected 50% to 60% from their highs. If the broader market does turn down, these are exactly the kind of areas that hold up best while still offering attractive yields. Being sector-aware rather than just yield-chasing is one of the most important shifts an income investor can make.

The other insight is that yield can serve as a buffer. A high-yielding stock with strong technical support gives you a 10% cushion against capital loss, which means a well-timed entry can deliver both income and capital appreciation. The misconception that you must choose between income and growth simply is not true when you understand how to read price action.

Tower Limited (TWR)

Tower has been in a long-term decline, but the recent base testing followed by a strong acceleration above the trend angle is exactly the kind of pattern that signals a meaningful turnaround. Currently offering an 11.9% yield, the stock has come back to retest support and is showing real resilience around the $1 level.

The technical picture suggests waiting for the current correction to play out before committing fully. As long as price holds above the $1 mark, this looks like a constructive setup, and the upside potential to the $1.80 region represents a 20% capital gain on top of the dividend. The key resistance to clear is the previous high zone, where the stock has met selling pressure once before. A clean break opens the door to far better risk-reward.

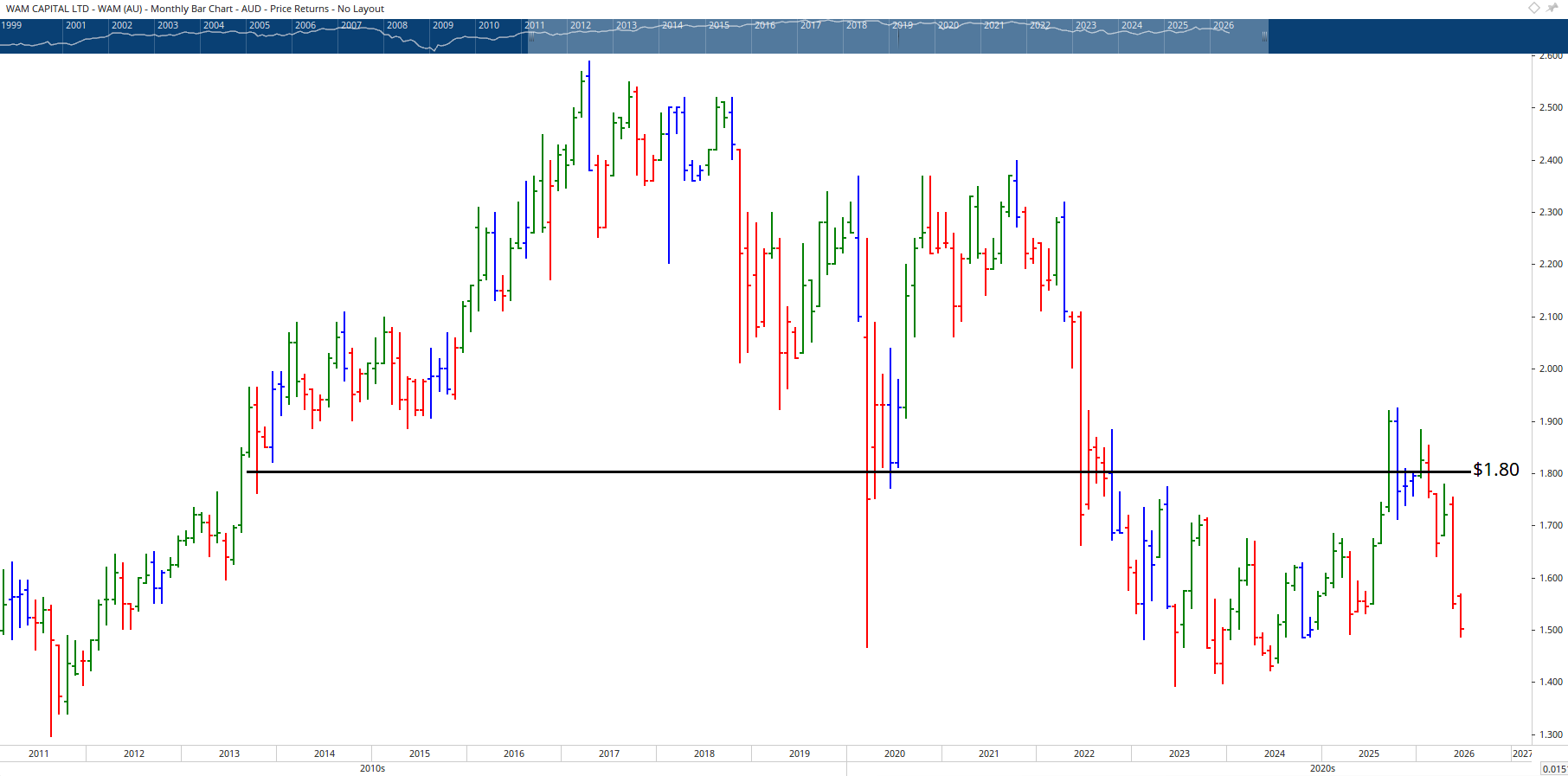

WAM Capital (WAM)

WAM Capital is offering a 10% yield, roughly double what major bank term deposits pay. For investors thinking about parking cash, this is a fundamentally different proposition with capital growth potential layered on top.

What makes WAM particularly interesting is that the share price has effectively returned to 2002 levels. Throughout history, this stock has gravitated back to exactly this price zone, which means buyers stepping in here are getting a price they may not see again for years. The most recent comparable opportunity was during COVID, and that window closed quickly.

In the short term, the stock looks opportunistic at current levels. For investors wanting more confirmation, a break through the $1.80 to $1.90 zone and a clean move past the downward momentum line provides far more conviction. Either way, the combination of long-term price support and a 10% yield is a rare combination at this level.

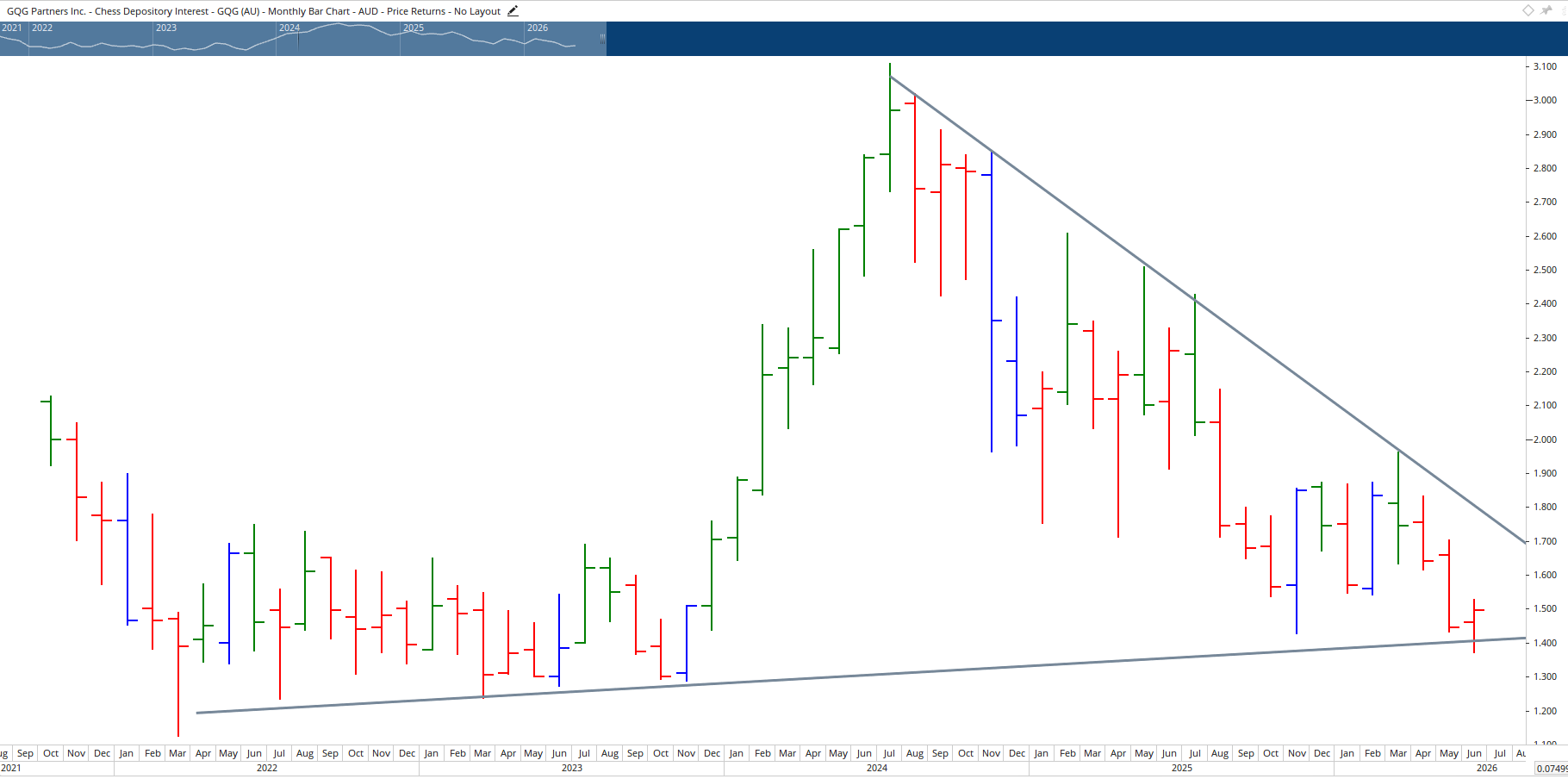

GQG Partners (GQG)

GQG Partners is a Chess Depository Interest currently offering a 10% yield. The stock has returned to a long-term technical level that has consistently provided support, and the way it is unfolding mirrors the base patterns that often precede sustained uptrends.

A simple trend line drawn from the lows provides a reasonable framework for managing risk. The stock is currently trading between $1.40 and $1.50, with overhead resistance that has rejected the price multiple times. Some traders may look to enter early on a break of the immediate trend line, while more conservative investors will wait for confirmation above the resistance zone. Either way, the yield provides a meaningful buffer while the technical picture develops.

The cautionary note here applies to all high-yield stocks. The temptation to hold simply because the yield is generous can blind investors to deteriorating price action, so always be willing to act if the technical picture changes.

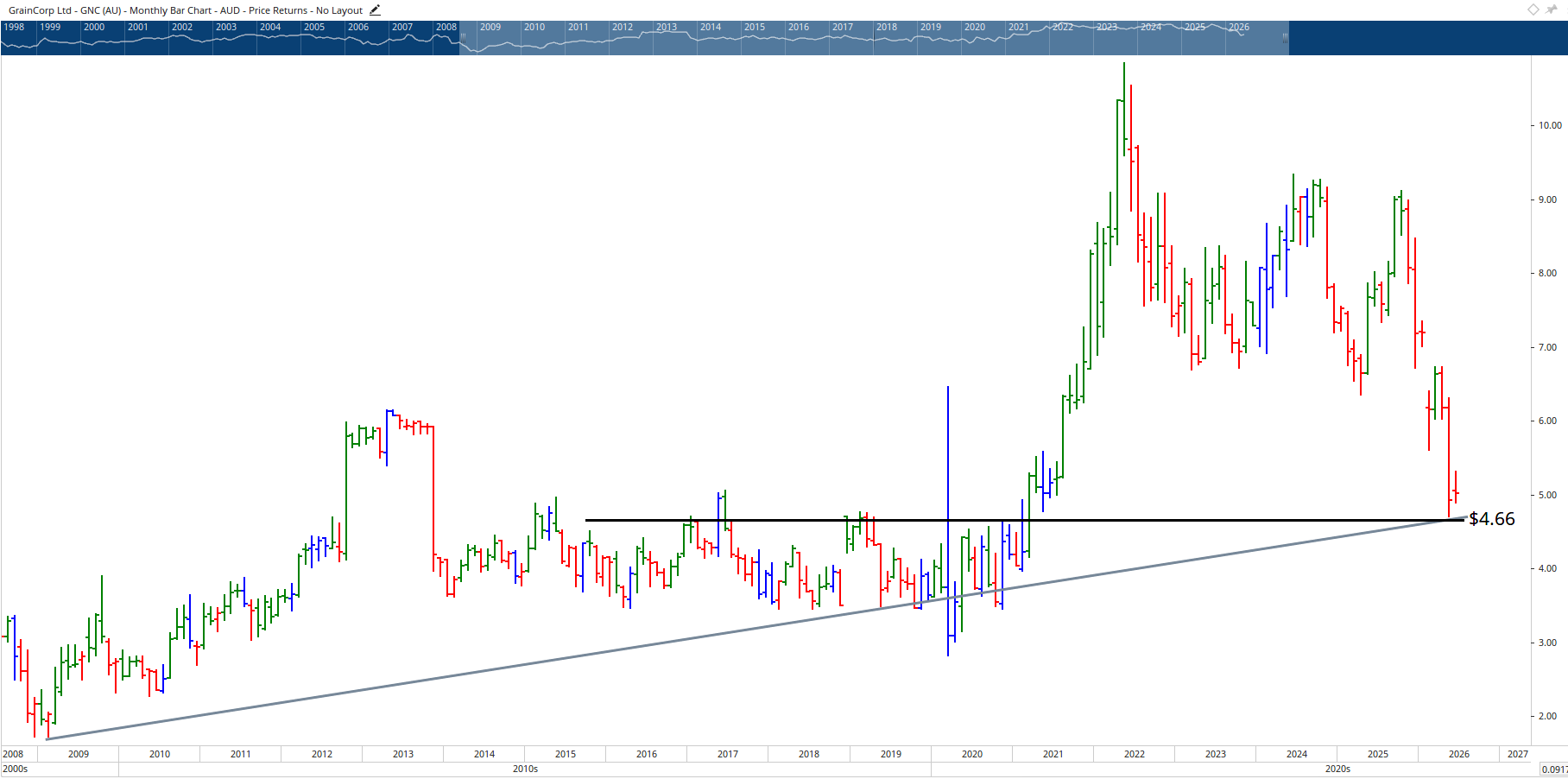

GrainCorp (GNC)

GrainCorp is the standout of the bunch. This is a deeply cyclical business that has spent significant periods reverting back to the long-term trend, and right now the stock is sitting at one of the most important technical levels in its entire history at $4.66.

Currently paying a 9.6% yield, this stock's historical correction pattern is remarkably consistent. Previous corrections of 60% and 58% set the precedent, and the most recent correction of around 55% falls within the same range. For investors seeking income, this combination of major support, a generous yield, and a textbook cyclical pattern stacks the odds decisively in their favour.

This is not necessarily a buy at today's prices, as the most professional approach is to wait for genuine confirmation that the bottom has been established. But as a stock to be watched closely with a view to entering at the right moment, GrainCorp is among the most compelling income setups currently available on the ASX.

Trending Topic: Bird Flu and the Risk to ASX Markets

Bird flu has arrived in Australia, and the market is rightly asking whether this poses a serious threat. The answer depends entirely on whether the outbreak escalates into something more significant or remains contained. Australia successfully managed a different strain in 2024, but the current strain is materially more dangerous and has caused major disruptions overseas.

If the virus reaches commercial poultry farms, supply shortages, higher food prices, and pressure on consumer staple stocks like Woolworths, Coles, and particularly Inghams, become realistic outcomes. The historical precedent is the 2006 banana inflation shock, where prices surged 250% in a single quarter and added around 0.5 percentage points to quarterly CPI. A similar chicken-and-egg dynamic could meaningfully delay rate cuts at exactly the moment the market is positioning for them.

Inghams itself is the stock most directly exposed. The company has locked down its Western Australian breeder farms, and the share price has held steady so far despite the news. Technically, the stock has been falling for a decade and is showing the kind of base-building behaviour that often precedes recovery. If management contains the outbreak successfully, a recovery toward the $2.40 level becomes plausible. If the situation escalates, the recent low remains at risk. This is a watch rather than a buy, but the setup is worth tracking carefully.

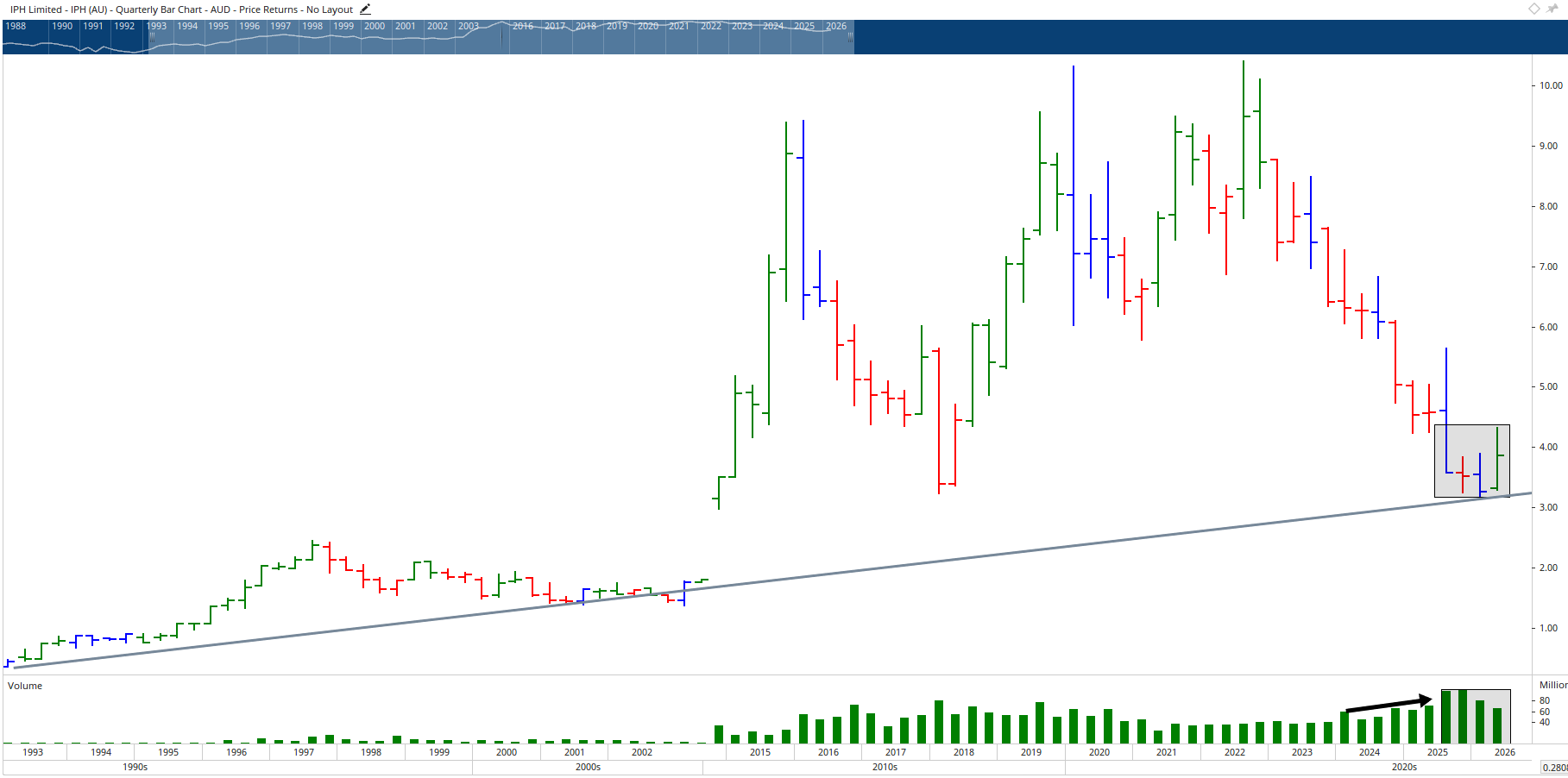

IPH Limited (IPH)

IPH is offering a 9.5% yield and sitting at a critical long-term momentum level. Unlike Inghams, where buyers have yet to step in decisively, IPH is showing clear signs of buying, with price already pushing through key levels.

The stock appears to have undergone a stock split adjustment, and the price is now testing whether the recent momentum shift can hold. Volume is picking up through the lows, which is constructive. If the stock can clear the immediate resistance zone, the technical picture becomes notably stronger. With a near 10 % yield providing a buffer, this is one of the more interesting setups in the financial sector right now.

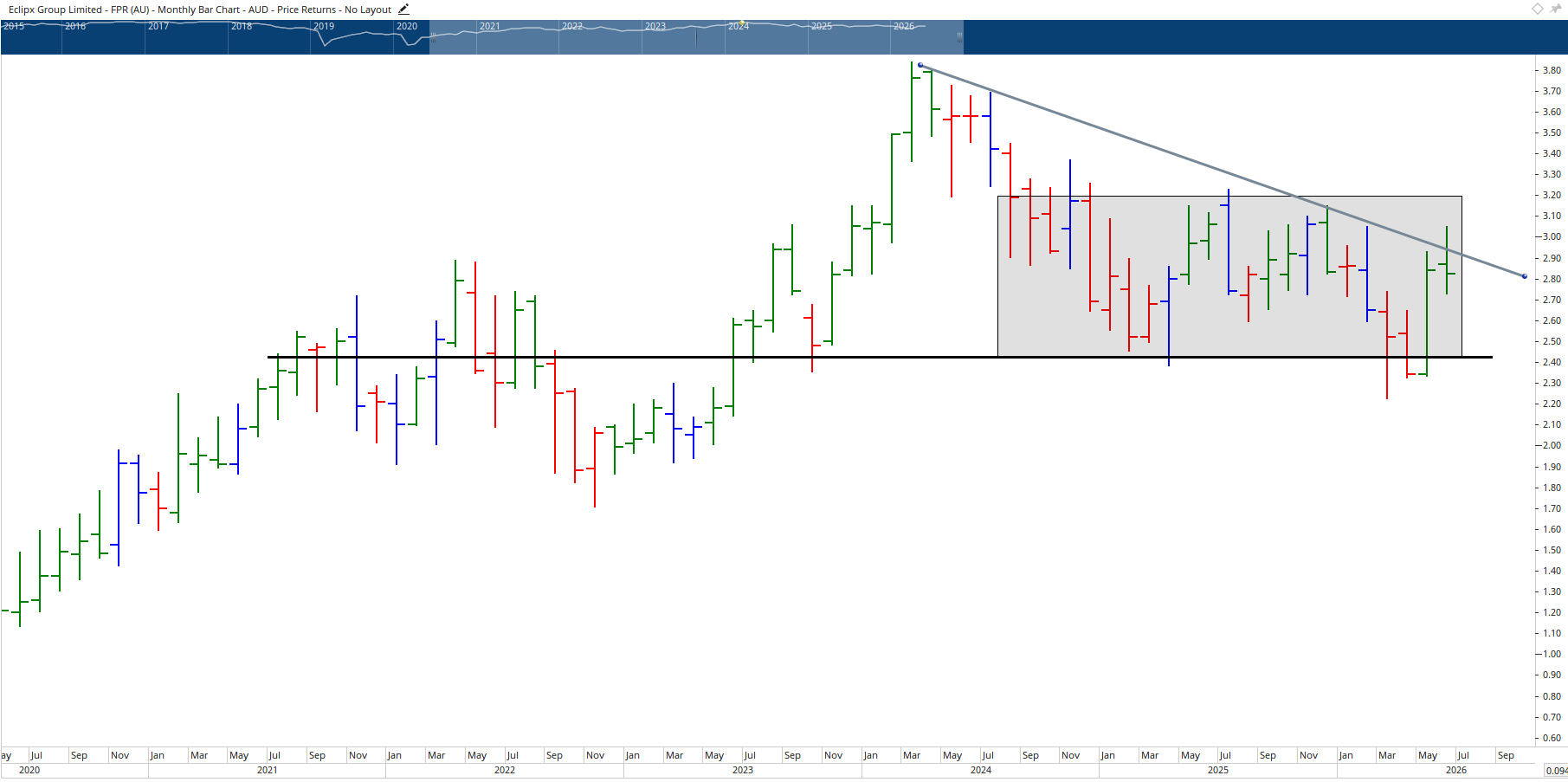

Eclipx Group Limited (FPR)

Eclipx Group is showing a classic compression pattern at long-term support, with a 9.2% yield attached. The buyers and sellers have reached a stalemate, and the price is forming an apex that will eventually break in one direction.

Patient investors should wait for the retest to complete and confirmation of direction before committing. The stock tried to push through the trend line but closed back down at support, signalling that profit-takers are still active. This is exactly why direction matters more than yield. Buying on the basis of the dividend without confirmation of a turn would be a high-risk approach.

Magellan Financial Group (MFG)

Magellan has been widely discussed after the enormous correction from the all-time high. Like several other stocks discussed in this episode, the structure now shows price moving back to the long-term trend and basing out, which is the same pattern that often precedes major upside moves.

If the stock starts moving up and convincingly breaks the $12 level, a path back toward $30 becomes realistic. This is a contrarian play, given how poorly the stock has performed over the years, but the technical setup is compelling. The critical risk management rule is simple. If price breaks below the May or June low, the trade idea is invalidated, and there is no reason to hold. With those parameters in place, this is one of the more interesting recovery stories on the ASX.

ARB Corporation (ARB)

ARB has come back to a beautiful long-term angle that has held since March 2020, around $10.60 to $10.70. The current pullback has tested but not yet fully confirmed the support, so patience is warranted.

The 8.8% yield provides a reasonable buffer, but the smarter approach is to wait for a proper confirmation of the test before entering. If support holds and price clears the immediate resistance, the next upside target sits around $26. ARB operates in the automotive accessories sector, which benefited heavily from the post-COVID surge in caravans and four-wheel drives, and the business's long-term growth trajectory remains intact.

Reader Questions

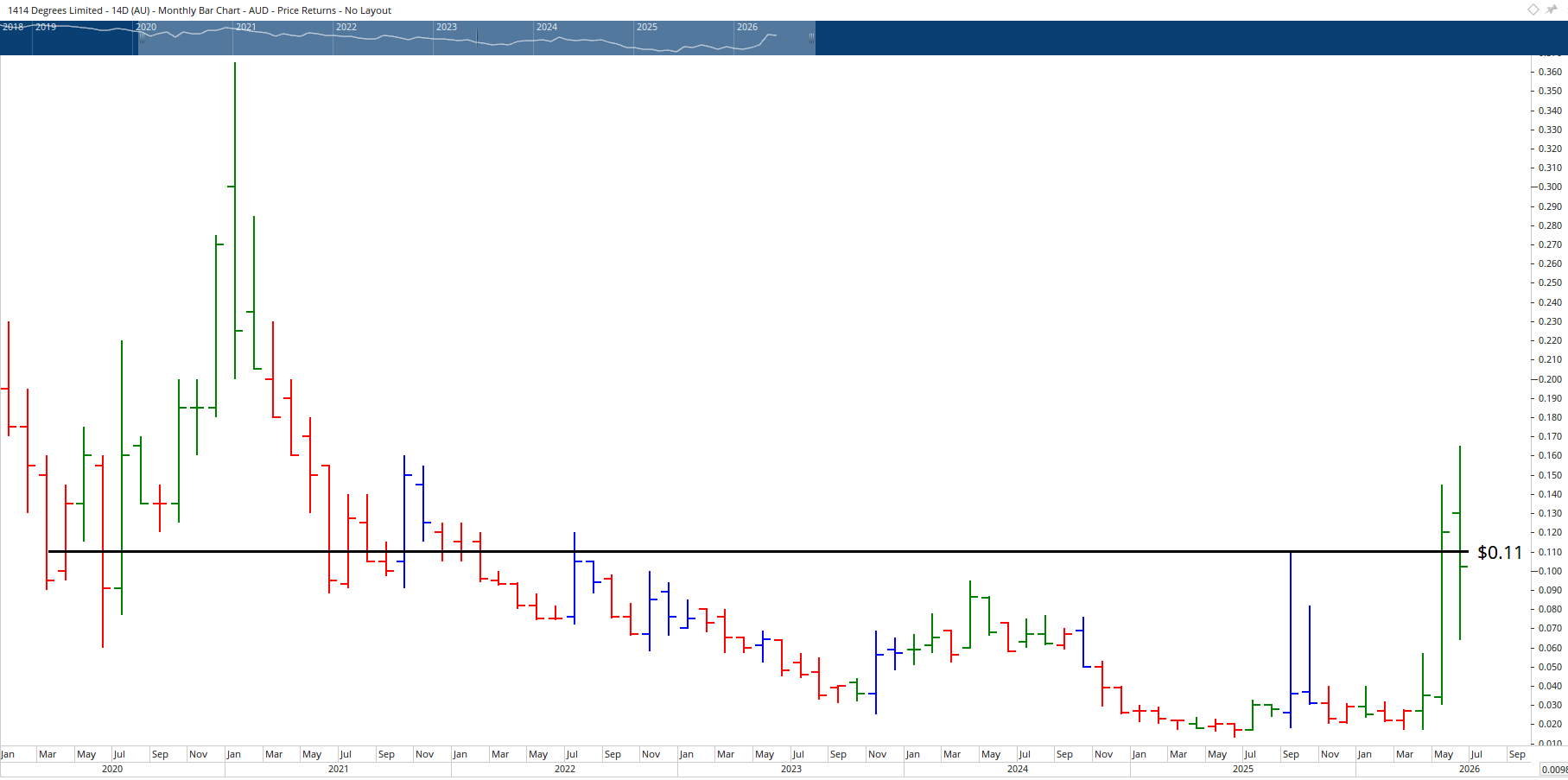

1414 Degrees Limited

Peter asked about 1414 Degrees Limited after buying in May and adding more in June. The technical picture here is concerning. The monthly chart shows no genuine uptrend, only sharp spikes followed by equally sharp falls. This kind of erratic price action, without a clear directional structure, is closer to speculation than to investment.

Before getting excited about this stock, investors would want to see the price at least begin to resemble a genuine trend, with sellers attempting to push it lower but failing. A close above 11 cents with a higher low forming behind it would be the minimum requirement. Right now, the price behaviour suggests this is a stock to monitor rather than commit capital to.

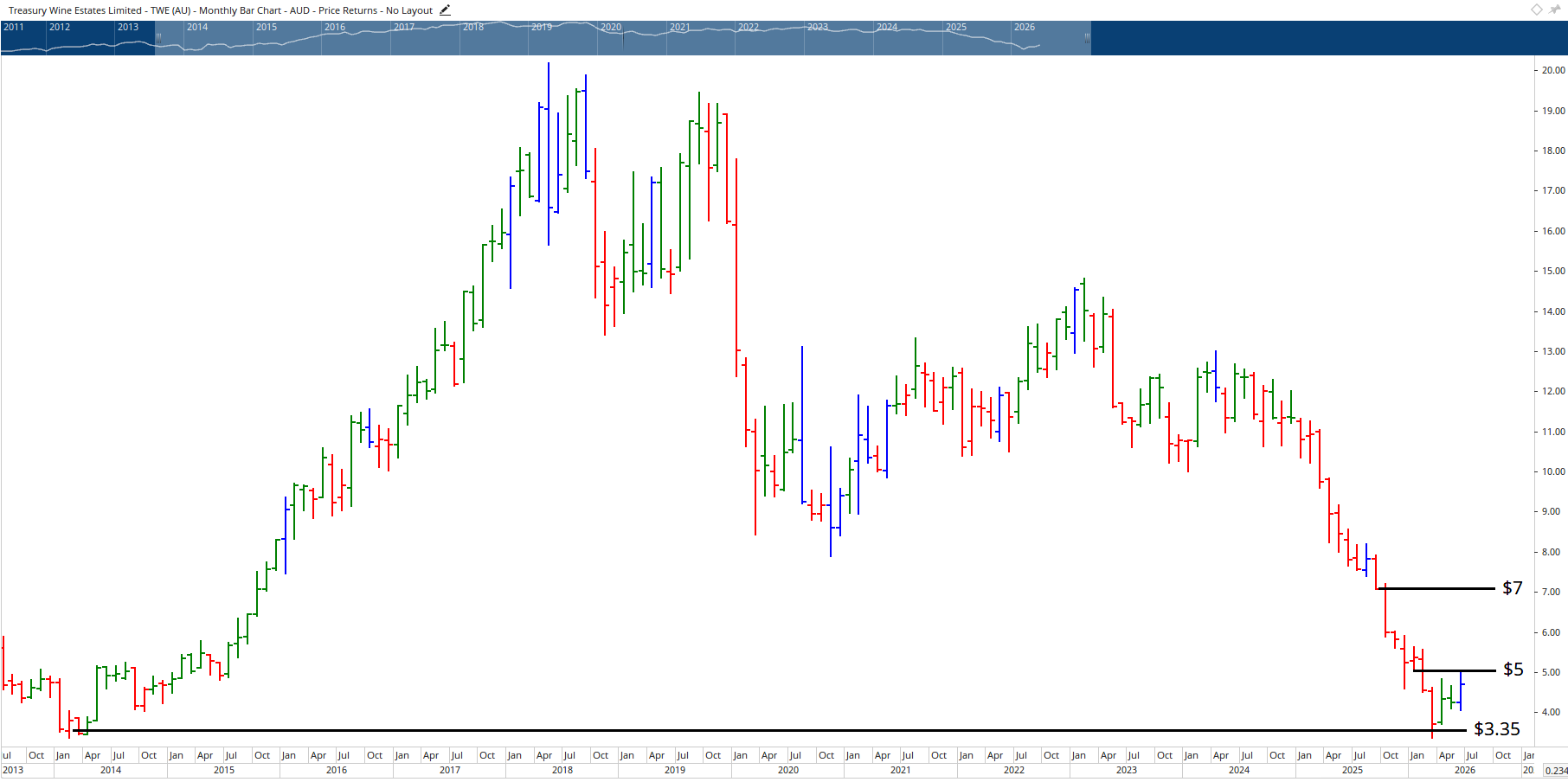

Treasury Wine Estates (TWE)

Brijesh asked about Treasury Wine Estates, identifying the $3.35 level as a strong historical zone and planning to enter on a break above $5, with a stop loss below the outside bar low. This is a textbook example of disciplined trade planning, exactly the kind of thinking that separates structured investors from speculators.

The monthly chart suggests the stock could be coming off the bottom, but has not yet done quite enough to confirm the turn. The weekly chart looks more constructive, with a potential pullback toward $4.50 followed by a break higher, offering an upside target of $6.80 to $7. The risk to be aware of is that the test of the low may not yet be complete, with prior resistance visible to the left of the price. The stop loss is well placed, and the plan is sound.

How to Get Started With a Small Capital Base for a House Deposit

Rex asked about using the stock market to grow a deposit for a house, with a focus on medium- to long-term growth. This is increasingly the only viable path for younger investors, given how little interest bank accounts now offer.

The fundamental advice is to keep the timeframe big and look at the market on monthly and weekly charts rather than daily noise. Rather than trying to identify a sector first and then stocks within that sector, watch a list of around 100 quality stocks across all sectors. This way, no opportunities are missed regardless of which sector is performing well, because individual stocks within weak sectors can still deliver excellent returns.

Once the charts are set up properly, monitoring 100 stocks takes only 10 to 15 minutes a week. Trade the stock, not the index or the story. News is the last to know, so filtering on news is one of the fastest ways to miss the best entries. Charts get you to the party early, while news is the signal that the party is already over.

Hot Stock Tip: Reliance Worldwide Corporation (RWC)

Reliance Worldwide Corporation announced today that it is shutting its Melbourne brass manufacturing operations and shifting more production to lower-cost suppliers and US facilities. The one-off accounting hit of around $100 million in financial year 2026 is largely non-cash, and management expects the changes to boost annual EBIT by approximately $9 million from financial year 2027 onwards.

This kind of cost-cutting story has played out positively for several other ASX names recently, including Wesfarmers and Guzman y Gomez. The market typically rewards companies that cut deadwood decisively rather than letting underperforming operations bleed value indefinitely.

Technically, Reliance is sitting at a hugely significant level around $3, which has been the long-term base. The stock has now pushed out above the recent downward trend line, and buyers were stepping in even before today's announcement. If the historical pattern holds, the next major upside target is $6, representing around 50% capital growth on top of dividends. Some retesting of the broken trend line before the next leg up would be ideal, but the combination of major support, an improving earnings outlook, and a clear technical structure makes this one of the more attractive setups on the watchlist.

The Real Insight: Direction First, Yield Second

The thread running through every stock discussed in this episode is the same. The highest yields are not the safest yields, and the dividend percentage tells you very little about whether a stock is worth owning. What matters is the direction of the price action, the technical support behind the share price, and whether the company has the operational quality to keep paying through cycles.

Most income investors fall into the trap of chasing the largest dividend they can find, only to lock themselves into a falling share price. By the time they realise the dividend was a red flag rather than an opportunity, the capital loss has wiped out years of yield income. The skill of reading price action first and using yield as a secondary filter is what separates investors who build wealth from those who slowly erode it.

This is exactly what we focus on at Wealth Within. Our stock trading courses are built around teaching you how to read these setups for yourself, so you are never reliant on someone else's view to make confident decisions about your own portfolio.

For those starting out, the Short Course in Share Trading provides the foundational skills needed to read charts, identify trends, and manage risk. If you are ready to commit to a comprehensive, government-accredited program, the Diploma of Share Trading and Investment teaches the full five-step approach used by professional traders. And for graduates wanting to refine their edge with techniques like time analysis and Elliott Wave, the Advanced stock trading course is the natural next step.

Final Thoughts

Big dividends and big growth rarely line up at the same time. When they do, it is almost always because a quality stock has corrected back to long-term technical support, dragging the share price down and pushing the yield up while the underlying business remains intact. That is exactly the environment we are seeing across multiple ASX names right now.

GrainCorp stood out as the strongest setup in the discussion, with cyclical support, a 9.6% yield, and historical precedent all aligning. Magellan, IPH, and Reliance Worldwide all offer compelling combinations of yield and capital recovery potential. The opportunity for income investors is genuinely rare, but it requires the discipline to read direction first, treat yield as a buffer rather than a target, and commit only when the price action confirms the setup.

As always, the difference between catching these opportunities and watching them pass is education, structure, and patience. With the right framework, you can stop chasing the highest yield on a screen and start building an income portfolio that actually grows your capital while paying you reliably along the way.

Disclaimer: This article is general in nature and does not constitute personal financial advice. Always conduct your own research or consult a licensed adviser before making investment decisions.